Cash Out Refinance Letter Sample [Tips & Sample]

This article will provide a step-by-step tutorial and two examples on how to create a Cash Out Refinance Letter.

Lenders don't usually need a letter of explanation for a cash–out refinancing. However, it may aid them in better understanding your requirements and position.

Under certain instances, it can even determine whether your application is accepted or rejected. So, whether or not you're asked, it's a good idea to attach a letter.

And how to draught a stellar letter of explanation for a cash–out refinancing that will help you get accepted.

What is a cash-out letter for refinance?

A Cash-Out Refinance Letter is made sent by a mortgage debtor who wants to leverage the equity they've created to their advantage and replace their previous mortgage with a new one, getting a lump amount of money to go toward renovations, paying off debts, or dealing with other financial concerns.

To persuade the mortgage company to allow you change the conditions of your home loan, you must explain your goals and demonstrate that you have enough equity in your property to justify a possible refinance.

Do you have to report cash-out refinance?

On a cash–out refinancing, some lenders almost always need a letter of explanation. Others will only need a letter if they are undecided about whether or not to accept your remortgage.

Within this situation, the letter of explanation is your last chance to win the case. As a result, take it seriously.

Your application's layout, spelling, and language can all reflect negatively on you. So take your time, double-check your spelling, and have someone you trust edit your message for errors.

You may also run a draught past your loan officer to make sure it's exactly what the lender needs before submitting the final edition.

- If your lender demands it, you must always give a letter of explanation for a cash–out refinancing. You have no choice except to cancel the application and go.

- If the mortgage underwriter perceives your application as borderline and requires some assurance about what you'll do with the money, you'll likely receive such a request. However, some lenders make these inquiries for all applicants automatically.

READ:_ Letter To USCIS Sample

How to write cash out refinance letter?

Consider your letter to be a marketing opportunity. You're attempting to persuade the reader to "believe" your justifications for borrowing. And your reader is a mortgage underwriter, who accepts or denies loans depending on their estimate of your borrowing risk.

You should endeavour to put yourself in the readers' shoes, as you should with any excellent marketing message. Then say exactly what they want to hear.

As a scenario, you can remark that you wish to make an investment in your house by upgrading the kitchen. You've received three remodelling cost estimates and are attaching your favourite. Explain any discrepancies between that amount and the one you've applied to borrow.

Whether you're borrowed too little, explain how you'll make up the difference. Alternatively, if you're borrowing more than the quoted amount, specify where the remainder will go. You might wish to put it in your emergency reserve for rainy days.

It's usually not a good idea to suggest you're spending the money on a one–time extravagance, such as a trip or a high–end automobile. Consolidating other high-interest obligations, on the other hand, is good.

Ultimately, you must never, ever, ever, ever, ever, ever, ever, ever, ever, ever, ever Because your cover letter is a required component of your application. Mortgage fraud can also be turned into a federal case by prosecutors.

From the top of the page to the bottom, here's a list of the things you should include in your letter of explanation:

- Lay out the letter as you would any other, starting at the top with your complete street address and phone number.

- Date the letter according to the date you're writing it.

- Fill in the recipient's (lender's) complete name and address.

- Add a greeting — How you greet your reader isn't important: "To whom it may concern," "Dear underwriter," "Dear Sir or Madam," "Dear Underwriter," "Dear Sir or Madam," "Dear Sir or Madam," "Dear Sir or Mad You make the decision.

- "Re: Cash–out refinancing application for [your and any joint borrower's complete names]," the next bold header reads. Your reference: [the number assigned to your application]"

- You're finally able to start writing your content. Begin by describing the letter's objective. Then, in the following paragraph, supply the needed information.

- Make certain you respond to the question that has been asked. However, make it brief.

- Add a closing line - "Sincerely," for example.

- Make a space on the page for your signature (s)

- Fill in your complete name and the names of any joint borrowers below that gap, as well as your email addresses and phone numbers.

Make sure you and any co-borrowers sign in the spaces you've left for signatures.

Also, provide any supporting materials you believe may be beneficial. It's important to remember that it's in your best interests to come across as completely honest and open.

Cash out refinance letter sample

1. Cash out purpose letter sample

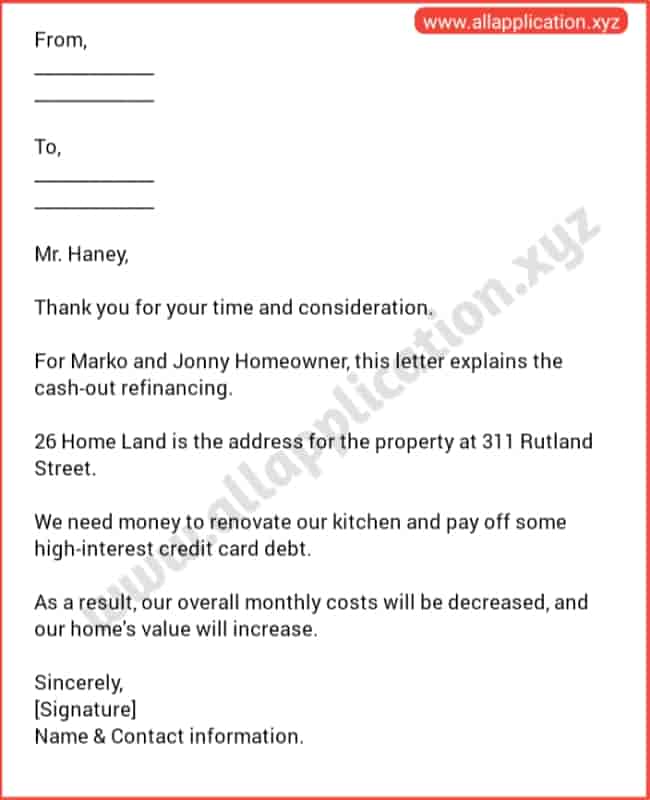

From,__________________________To,_______________________________________Mr. Haney,Thank you for your time and consideration.For Marko and Jonny Homeowner, this letter explains the cash-out refinancing.26 Home Land is the address for the property at 311 Rutland Street.We need money to renovate our kitchen and pay off some high-interest credit card debt.As a result, our overall monthly costs will be decreased, and our home's value will increase.Sincerely,[Signature]Name & Contact information.

2. Letter of explanation for non payment

RE: Mortgage Loan Application of Jessica SmithDear Hallen,I'm writing to explain the late payments on my American Express credit card, account 900795, dated 15th January to 18th October 2022.Due to the COVID-19 pandemic, I was let off from my work on April 15, 2022. I was unable to make my minimum credit card payments for this account in May and June due to my unemployment. On June 20, 2022, I started a new job and was able to make my July payment.I'm still working for the same firm now, and I haven't missed or been late on a payment on this credit card account since July 1, 2022.As confirmation of my excellent standing and on-time payments with this account, I've included a copy of my statements from July 1, 2022 to the present.Sincerely,

Related articles:-

![Application to Police Station for Lost Mobile Phone [5 Samples]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEhXhJ6SmjGJCff4RkwNd4ZIuhP_wkYbzedpfRSyQsE5vwUNP3SrwhjBXroU18z5hmBncjCy183Nxd5zT8rc0iKC0F_WuokKLOJQOzrS0KZfGyJaamuXdA2aCoVgL_dH24e4SY0j3ktwtvO_/w72-h72-p-k-no-nu/Webp.net-compress-image.jpg)

![Half-Day Leave Application for Doctor Appointment [5 Samples]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEhsapKsC7-Dem8dDajdEeYalCayjHPGKJZboIFXr6ISujMHa57VQStIJNcv88WAAFmOnxwMXCOi6-eTYldLcCqHWrTEYgXOyrFOvKjXNN3gFGPLRdFbDlTwKX23sNjSDOmaNyn1GQ9mLUc/w72-h72-p-k-no-nu/20210410_085952.jpg)

0 Comments